Social Security Secrets

This message is NOT approved, endorsed, or authorized by the Social Security Administration. All information regarding Social Security discussed or mentioned here is available for free from the Social Security Administration.

What if You and Your Spouse Could Get an Extra $111,000 in Retirement?

You Could Lock in Six Figures in “Extra” Social Security Benefits Over the Course of Your Golden Years

Just 4 out of every 100 retirees claim their maximum retirement benefit.

This REVEALING BOOK shows you strategies that could hand you tens of thousands—or even $100,000 or more—in EXTRA dollars, funds you have to know when—and how—to ask for.

Dear Reader,

Chances are, you qualify for extra money from Social Security but don’t realize it.

If you’re already collecting benefits, you may be eligible for tens of thousands more.

If you’ve not yet claimed your Social Security—now’s the time to get the lay of the land so you can maximize what you’re eligible for and minimize the taxes you’ll pay on it.

According to a recent study, just 4 out of every 100 retirees are claiming the maximum they could. That means a whopping 96% of retirees could be pocketing more each month. They don’t claim at the right time to maximize what they could receive or else there are additional benefits they’re eligible for—based on birth date and marital status, for instance—that they don’t realize they can request.

That’s additional money that could be spent on anything from living expenses to meals out every week to annual beach vacations or even trips abroad.

Or these extra funds could simply be that cushion you need to secure a worry-free retirement. Now more than ever—with the uncertainty surrounding the Covid-19 shutdown and the economic situation we’ll find ourselves in as this craziness begins to wane—it’s important to understand how you can be most strategic about how and when you claim your Social Security benefits.

Because we're not talking chump change that’s in play here. The average retiree household leaves $111,000 on the table over the course of their retirement. Money they simply never see.

To put it plainly: This could be the difference between pocketing, say, the average retiree benefit of $1,548 a month, or as much as $3,895 a month—which some people will receive.

“Even a minor Social Security misstep can rob your nest egg of tens of thousands of dollars in retirement benefits.” – MoneyTalkNews

We’re talking about just over $18,500 a year in Social Security benefits versus more than $46,000 a year.

I don’t need to guess which end of that spectrum you’d prefer to be on. And let me just say, for the record—and I’ll get into this more in a minute—but yes, even in what are likely to be the economically challenging times of the post-pandemic period—Social Security is going to be there for you. (I explain why, below.) So it is well, well worth your attention now.

The good news is: All sorts of provisions and rules exist that can allow you to increase what you receive. In the brand-new 2024 edition of my book—I show you how to explore your options.

Let me give you an example:

This Couple “Found” $70,000

Consider Laura and Bob. They’re both 67 years old. Laura started to collect her Social Security benefit when she was 63—collecting $570 per month. Bob started his when he turned 66—and he collects $2,200 a month.

But what this couple did not realize is that they should, in fact, have been collecting more.

They didn’t know to ask if they were eligible.

You see, not all Social Security benefits are automatic. It’s up to you to request the funds you’re due—and you don’t know what you don’t know.

My name is Steve Garfink—I’m the author of Social Security Secrets: How to Maximize Your Income for a Worry-Free Retirement and I hold a National Social Security Advisor Certificate and am also Certified in Social Security Claiming Strategies, and hold the Certified in Social Security Claiming Strategies (CSSCS) designation..

Social Security is complicated. Sometimes the rules work in your favor and sometimes they don’t. But forewarned is forearmed.

Take the “Tax Torpedo,” for instance. Never heard of it? You’re not alone. Most investment advisors and retirement planners are unlikely to explain this to you since it runs against the grain of their primary advice: Avoid drawing down from your tax-deferred accounts as long as possible.

Your Social Security is subject to preferential tax treatment under IRS rules. In fact, lots of people will never pay any income tax on their benefits. However...others WILL pay tax. And that’s where the “Tax Torpedo” comes into play.

Once your other income—apart from benefits—exceeds a certain level, then for each additional dollar of such other income, up to $0.85 of your benefits become taxable. Think about that for a moment: $1 of “other” income results in $1.85 of taxable income.

Yikes. In Social Security Secrets: How to Maximize Your Income for a Worry-Free Retirement I explain how it works in detail—and show you how you could avoid it!

When Laura and Bob followed a bit of guidance I share in my book, they were able to take advantage of a provision in the law they’d never heard of before.

Turns out that Laura should have started collecting $905 a month after Bob filed, an increase of 59% in her benefit, or $335 extra per month. Yet for some reason that adjustment in Laura’s favor did not happen.

So the couple contacted the Social Security Administration and, having reviewed the situation, the SSA corrected Laura’s claiming basis. They credited her for six of the 16 months since Bob had filed, and an additional $2,010 showed up in her bank account in one lump sum.

However, the other earliest 10 months she should have been collecting more—those funds were lost because, well, that’s the rule. Laura and Bob are out $3,350 because they were not aware of this provision earlier.

Still, they were thrilled to get an entirely unexpected $2,010 at once, plus $335 more per month. That’s $4,020 more each year!

If Laura and Bob each live to their average life expectancy of 85, they will have collected over $70,000 more, just because they got smart about exactly how the Social Security system works.

I share this story because you could find yourself in Laura and Bob’s shoes.

As I said before: You don’t know what you don’t know.

You Could Be Eligible to Receive Up to $50,000 in Extra Benefits

And that’s why I wrote my book, Social Security Secrets: How to Maximize Your Income for a Worry-Free Retirement. Because I wanted to lay out—in plain English—the important facts and show you how to take full advantage of the opportunities to maximize what you’re due without having to comb through the Social Security website.

Whether you’re already receiving Social Security, eligible to collect it soon, or that time is still a decade or two away. It’s important to understand your options.

But before I get to that, let me say: When it comes to maximizing the Social Security funds that are due to you, time is of the essence.

And this is true whether you’re already collecting Social Security, will be soon, or it’s still on the distant horizon. It really can pay—and pay big—to simply be informed.

In fact, if you are 66 or older, right now, you could be one of hundreds of thousands of Americans eligible under a specific provision to receive as much as $50,000 in additional Social Security over the course of your retirement if you meet the right criteria, but you have limited time to claim it.

|

Meet Author and Social Security Expert, Steve Garfink

Steve Garfink, author of Social Security Secrets: How to Maximize Your Income for a Worry-Free Retirement brings to the table 40 years of work experience in finance, strategic planning, and management. He holds a National Social Security Advisor Certificate and is also Certified in Social Security Claiming Strategies. Steve speaks regularly about smart Social Security strategies at International Living’s conferences and with financial planners, helping them to better serve their clients. He’s helped hundreds of readers like you to understand the options available and to maximize the Social Security income they have coming. You have more control over your retirement than you may think—and Steve shows you why that is and how you can best capitalize on it. Whether you’re already collecting Social Security, will be soon, or it’s still a decade or two ahead—it’s worth your while to get informed. You don’t know what you don’t know—and having a smart plan in place could be worth tens of thousands of dollars to you—or even more. |

You or your spouse (or any of your friends) could well be due these funds. In fact, even if you are divorced but were married for at least ten years, you could qualify for this benefit.

But you have to take action now.

You have to get in touch with the Social Security Administration—sooner rather than later—if you want to claim the maximum benefit available to you.

And it's up to you to know if you're eligible to receive this payout. It’s not automatic.

This particular provision relates to a significant Social Security loophole. A patch was made to it in 2016, which locked out a certain number of people—but hundreds of thousands more could still benefit from extra payouts…quite possibly you among them.

But in order to claim as much as $50,000 in EXTRA income—if you qualify—you have to know you’re eligible and you have to file a claim to request it. Just like Laura and Bob had to know to ask.

Now I want to be absolutely clear: I don't have anything to do with the Social Security Administration. And, in truth, the Administration has comprehensive information about this—and all their programs—posted online for free.

You are more than welcome to go ahead and wade through it. There's nothing to stop you from figuring out your eligibility on your own.

Their publications are available to you if you have the hours and the patience to spare. And you could, certainly, call an agent on the phone to inquire as well…

But the thing is…when it comes to this particular benefit, you have limited time to put in a claim for it if you qualify. Hesitate and you may well end up with only a partial payout—or none at all.

So for the sake of your retirement…don't delay!

I'm talking about regular payments—extra money you simply have to request in order to receive. It could be an extra $1,505 paid to you, month in and month out, for four full years, for example.

Just think about what you could do with that extra income in retirement. It could buy a better quality of life, mean more travel, or simply shore up your nest egg.

I'd be happy to email you all the relevant details. I’ve written an extra “Bonus Chapter” to my book, which focuses on exactly this provision and shows you how to know if you qualify and, if you do, exactly how to claim the extra funds that may be due to you, and I’d be happy to email it to you as a part of this special offer.

Your Timing is Critically Important—

and Can Be Worth Tens of Thousands of Dollars to You...or More

But understand that this provision is just one of many ways you can maximize the benefits due you from Social Security.

Experts estimate that the vast majority of people leave Social Security benefits on the table. Retired couples right now are missing out on an average of $111,000. Money that they could be claiming over the course of their retirement years.

They simply don’t take the steps necessary to maximize their benefit.

And that's the rub: You have to KNOW to ask. And you have to ask in the right way, at the right time.

But I can show you in plain English what you need to know in the pages of my book, Social Security Secrets: How to Maximize Your Income for a Worry-Free Retirement.

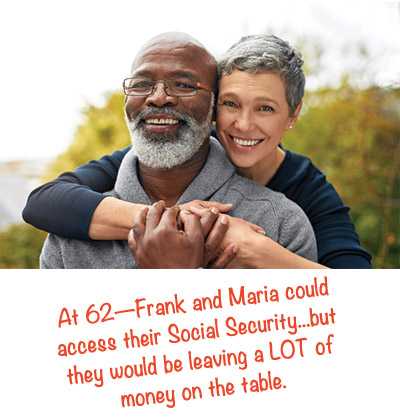

Consider, for instance, Frank and Maria:

They’re both 62 and want to retire. They could claim their Social Security benefits immediately—which would give them $2,700 a month (the equivalent of $32,400 a year).

So that’s one option—and they’re considering it.

But it’s NOT the smartest way to go if they’re interested in maximizing their Social Security and living worry-free over the long haul, as I explain in my book.

After all, the average older household spends $45,756 a year in retirement. They’d be starting out behind...

So what should Frank and Maria do instead? They’d like to start enjoying retirement—sooner rather than later.

Well, the good news is that they have some smart, nuanced options.

For instance, Frank and Maria could be eligible for “extra funds” from Social Security they aren’t currently aware of...they could put a “bridge plan” in place that would allow them to live well and enjoy life in that gap between now and their Full Retirement Age for Social Security purposes. I explore lots of options in my book in detail, in plain English, and with plenty of examples.

In fact, there’s a claims strategy Frank and Maria could make use of that would hand them about $4,700 a month in Social Security benefits (that’s $56,400 a year)—and, at the same time, they could watch whatever modest savings they have actually increase.

So instead of worrying they might run out of funds in their latter years, they could watch their nest egg grow as they age. (And this strategy assumes their savings do nothing more than keep up with inflation.)

By applying the secrets I reveal in Social Security Secrets: How to Maximize Your Income for a Worry-Free Retirement, instead of counting pennies and worrying they might outlive their funds, Frank and Maria could pocket a Social Security benefit that’s 76% more than what they would have claimed at 62. And with their nest egg expanding, they’d gain the flexibility and the comfort of worry-free years.

That is the power of having a claiming strategy that pays close attention to the timing of a claim and which takes into account your WHOLE retirement picture—not just Social Security in isolation.

In Social Security Secrets: How to Maximize Your Income for a Worry-Free Retirement I explore all kinds of scenarios with case studies and examples so you can see situations that might apply to you and understand how certain claiming strategies could work in your own retirement life.

Financial security over the long-term without any sacrifice to your lifestyle. That’s the end goal.

And rest assured that even in the wake of this pandemic, you’ll still have sound strategies at your disposal. We’re going to be facing a ravaged economy, and I’d argue that getting the most out of your Social Security is going to be more important than ever.

Financial Security: Your Social Security Is Just One Piece of the Puzzle

In my book, you’ll hear about how all kinds of folks—in all kinds of situations—can do it, by putting a smart Social Security claims strategy in place and by understanding how that Social Security claims strategy works as a “puzzle piece” of the bigger retirement picture.

For instance, I’ll talk about...

- How Gwen, a single woman with very modest savings who has had it with the cold and snow, could safely retire years earlier than she thinks she can and lock in that “endless summer” lifestyle she dreams about in Florida.

- How—after medical bills emptied Sarah and Stuart’s savings and he passed away too young—Sarah can safely recoup and make the best choices when it comes to Social Security’s survivor benefit. (Note: The survivor benefit is a double-edged sword and claimed incorrectly, the cost can be devastating.)

- How Diane and Curtis—who, lucky for them, have plenty of money saved—could make the most of their Social Security. If they do what their financial planner is telling them to, they’re likely looking at a “Tax Torpedo.” But there’s a MUCH better way to proceed, which lowers their tax bill and maximizes their Social Security.

- How Nora and Ted can rearrange the pieces of their financial puzzle to get at their goals faster, more securely, and with intangible benefits—like having their kids and grandkids close by.

- How Tracy, a single woman with no kids, could cleverly leverage the large family home where she lives (inherited from her parents) to put a smart claims strategy in place, which can quickly shore up her financial future so she doesn’t have to worry about ever running out of funds or being a burden on anybody.

- How Peggy and Ben—he recently left his job and she’d like to—could play with the idea of downsizing and how that, combined with their modest savings, could allow them to increase their Social Security benefit and retire earlier and better than they think they can.

- AND MORE... what sound (and attractive) choices Janet has when she loses her job at age 60... what Vanessa and Keith can safely do to “call it quits” at 62 and start living life... how Duke (a 34-year-old surfer) could put a claims strategy in place now, start surfing every day, and retire at least a decade earlier than he thinks he can...

How to Ensure You Can Enjoy Your Retirement, Worry-Free

Social Security can be complicated—I won’t pretend it’s not. But it’s not rocket science. There are simple, proven strategies you can make use of that will help you maximize what you receive.

You know, if you’re like me—and like most folks thinking about retirement—you have a few “umbrella” goals:

- You want to maintain—or even improve—your standard of living.

- You want to be able to afford to pivot to your “future life,” that retirement life you imagine in your mind’s eye, sooner rather than later.

- And you want to enjoy greater financial security as you age—so you never have to worry about running out of money.

Those goals may feel ever-more-distant in our current circumstances, but in Social Security Secrets: How to Maximize Your Income for a Worry-Free Retirement I’ll show you how you can put a plan in place that will deliver exactly that.

So you have the freedom to retire when you want, where you want, enjoy days that look the way you want them to look...and never have to worry that you’ll outlive your nest egg.

You Have More Control Over How Much You Get Than You May Imagine

When it comes to your Social Security benefits, you in fact have a lot more control over how much you receive than you probably think.

Most people assume that, after having paid into the system for all their working lives, the payout is pretty much automatic, within certain clear parameters.

But that is NOT AT ALL the case.

It's really up to you to navigate what is a genuinely a complicated system. Social Security has nearly 3,000 rules governing benefits…thousands of additional rules explaining that first set of rules…and a tangled web of red tape around claiming them.

At various junctures, you have opportunities to cash in—to secure EXTRA income.

But if you don't request it in the right way at the right time, you may automatically forfeit your right to certain funds.

I'm talking about funds that often add up to tens of thousands of dollars for a single person and even hundreds of thousands of dollars for a couple.

“Americans are woefully unprepared to take full advantage of the Social Security benefits they’ve earned.” – Yahoo Finance

That’s why I partnered with International Living to publish my book—because I wanted to get the word out there. And International Living is in the business of helping people get the most out of their retirement.

The truth of the matter is: Social Security—while you may think about it as simply a "safety net"—might, in fact, be the most valuable tool you have in ensuring your "golden years" are not just comfortable…but actually hand you a retirement better than you ever imagined.

I'd like to help ensure that's the case for you.

Take Advantage of This Special Book Offer on the Table Today

And that's why I'd like to send you a copy of the new 2024 edition of my book called Social Security Secrets: How to Maximize Your Income for a Worry-Free Retirement, which will hand you a blueprint for how to maximize the Social Security benefits you're eligible for. (Right now, it comes with a bundle of FREE extras.)

And when you request your copy of the book as part of this special offer, not only will it arrive at your doorstep in the mail—but I'll also email you the details about that provision I mentioned, which could hand you as much as $50,000 in EXTRA income if you qualify—based on your birth year and your marital status.

All the specifics are in my “Bonus Chapter,” and I’ll happily email the details to you just as soon as you request your copy of Social Security Secrets.

This book shows you how to put a plan in place that allows you to retire better, and quite possibly earlier, than you ever thought you could.

And frankly, even if you opt not to request a copy of my book, I strongly encourage you to review the complimentary materials the Social Security Administration provides about their benefits. Chances are you'll leave money on the table if you don't get informed about what you're eligible to receive.

That said, this valuable book is unlike anything else out there. I know. I wrote it because the guidance I found was, frankly, incomplete (and, in some cases, downright confusing).

I have more than 40 years of work experience in finance, strategic planning, and management. And when my wife and I were approaching retirement age, one of the first things I did was to turn my attention to sorting out our plan for claiming Social Security. I figured it would be a pretty straightforward task and one I was highly qualified to do.

Only I discovered that—despite an Ivy League education and my long professional background in finance—Social Security wasn't nearly as straightforward as I'd assumed.

So I dove into it with great focus, and today I hold a National Social Security Advisor Certificate and am certified in Social Security Claiming Strategies and hold the Certified in Social Security Claiming Strategies (CSSCS) designation.

Social Security is incredibly complicated. And, as I've said, the vast majority of people leave money on the table.

But you don't have to.

I put this book together to ensure you have the straight story. Again, I am not associated with the Social Security Administration. But I’ve done a deep dive into the minutiae of the system and I’ve come out with a strong understanding of how it all works.

The Baby Boomers who have heard me speak on this subject say in overwhelming numbers that they'd recommend my valuable insights and clarifications.

For lack of a better way to say it: I’m plain-spoken. I don’t believe in complicating matters. Social Security is complicated enough as it is.

Frankly, I pride myself on bringing a plain-English approach to Social Security.

Insights, Recommendations, Advice—Even Revelations—that Nobody Else Tells You

Here's the thing…part of the reason that what I have to say is so powerful is that basically NOBODY else is saying it. There's a lot of rotten, inaccurate information out there about Social Security.

“Your research showed me a way to do something that I had no prior conception of and gave me a new direction. Not only that, but the focus has given me new energy and excitement. It was a decidedly uplifting experience!” – L.E.

Not to toot my own horn here, but as my publisher said to me once, “People hear you explain the fundamentals of the claiming strategies you recommend…and it feels like a revelation.”

The advice I have to share isn't just eye-opening…it could be worth thousands of dollars to you over the course of your retirement.

Here's what you have to understand…

For starters, the good folks at the Social Security Administration, while they aim to be helpful, are busy—too busy.

Between 2010 and 2019, the administration’s operating budget fell nearly 11 percent in inflation-adjusted terms. They lost 12 percent of their staff over that period while the number of beneficiaries grew by 17 percent.

Workers are often hamstrung. There’s a backlog of behind-the-scenes work. And in the last decade, many field offices have closed while office hours have been shortened in the ones that remain open. All the while, roughly 10,000 Baby Boomers a day reach retirement age.

Now, the pandemic forced the agency—like so many other organizations—to adapt to doing business virtually. That’s been a positive development overall with increased services to the agency’s 800-number, more than 6,000 new frontline workers, and the availability of more phone and video appointments. No question, we’re seeing some much-needed improvement.

But that doesn’t change the fact that the benefits the agency provides remain complicated and it’s up to you to understand them.

It’s all just more reason to get a handle on your situation yourself—and my book is designed to help you do that.

A study done by the Government Accountability Office revealed that people looking for advice from Social Security employees about when and how to best claim their benefits weren’t getting key information they needed from employees to make well-informed decisions and maximize what they might receive.

The Social Security Administration has lots of information that's useful—but ultimately, it's up to you to dive in and navigate your way through it. It’s critical that you understand the lay of the land and know what questions to ask. And neither of those things are obvious.

The SSA website has more than 45,000 web pages. Meditate on that for a moment and you can see why I think it's useful for you to get some practical insights from somebody who has spent a lot of time under the hood.

Information is one thing. Knowing what to do with it is another entirely.

In Social Security Secrets: How to Maximize Your Income for a Worry-Free Retirement I translate the "facts" into practical, real-world guidance.

I am on a mission to show people how to increase their Social Security benefits…and plan for a retirement that's more comfortable—and often earlier—than they ever thought they could have.

In fact, in partnership with my publisher, we’re undertaking a national push to show as many Americans as possible that they have more power over the value of their Social Security benefits—and their retirement—than they probably think.

We Believe Strongly in the Promise of this Book…

Claiming your Social Security benefits at the wrong age and in the wrong way can cost you dearly.

Now there are plenty of folks out there claiming the proverbial "sky is falling" when it comes to Social Security. They'll tell you that you better grab your benefits as quickly as you can—the minute you're eligible—since there's no guarantee Social Security will be there in years to come.

In fact, it has become so common to question the viability of Social Security that it's difficult to know where to begin to push back against the assumption that it is bound to fail.

But push back we must…because this wrong-headed belief results in costly mistakes that are destroying the last—and most excellent—chance for Baby Boomers to establish a financially secure retirement. And once you understand how Social Security really works, you can use that knowledge to create the best strategy for the retirement you deserve.

I’ll show you how in Social Security Secrets: How to Maximize Your Income for a Worry-Free Retirement.

Let's start with the bottom line: The chance is exceedingly small that Social Security is going to run out of money, either for the 10,000 Baby Boomers starting benefits each day or for the Gen Xers and then Millennials following on their heels…

You Should Count on Social Security Being There for You

Social Security touches more people than just about any other federal program. And it is arguably the most popular government program in existence.

Enthusiasm for it holds up strongly across party lines with 93% of Republicans, 99% of Democrats, and 92% of Independents all agreeing that it’s an important program.

Which brings me to my point: Even though Social Security is incredibly popular—you might even say "beloved"—you get lots of people saying that it is on the chopping block…and that it's bound to fail.

But the dirty truth of the matter is this: When public figures tell us that something very dear to us is threatened, it gets our attention. Politicians speak hysterically about Social Security because it is a reliable path to votes and money.

Consider this: If you are a politician and you want to reach out to voters, which of the following appeals seems, well, more appealing?

Option A:

"Social Security is fine. Don't worry about it. Please vote for me and send me money."

Or

Option B:

"Social Security is going bankrupt. The [NAME OTHER PARTY] is out to destroy it. Together we can save it…if you vote for me and send me money."

Clearly, Option B gets more people's attention. And the press tends to repeat the "Option B" stories because "hysteria" sells more newspapers and magazines and page views online than "boring" stories do.

Those people directly threatened by the specter of an unstable Social Security system—and I'm talking here about the more than 69 million Americans receiving Social Security benefits right now—they fret and stew.

The other couple of hundred million who don't yet collect benefits…they certainly don't feel great confidence in the future.

Really, it's not surprising that we're all left with the impression of a program that is tottering like a boxer about to go down for the count.

So it stands to reason that people close to claiming their benefits might logically figure they had better do so as soon as they're eligible and collect before the system runs out of money.

Younger folks might understandably conclude that the program isn't going to be there for them, so why bother to plan for it?

But here's the thing: It's all nonsense.

The likelihood of Social Security going belly-up is incredibly thin. And if you panic and just collect as soon as you can in the most obvious way available to you, figuring you better "get yours while the getting is good," you are bound to lose out on tens—if not hundreds—of thousands of dollars.

The current bluster isn’t to be discounted—that’s not what I’m suggesting. It never hurts to send a note to your representatives and tell them how important you believe Social Security is. I am simply saying that, because Social Security touches so many people, it’s a topic around which tens of millions of voters are ready to rally. And because of that rallying, it’s not likely to disappear.

Social Security is "Off Course" But Readily Fixable

The truth of the matter is that Social Security is slightly "off course." And there are simple, reasonable ways to fix it, as I explain in detail in Social Security Secrets: How to Maximize Your Income for a Worry-Free Retirement, so I won't belabor the discussion here.

I'll simply say that recent forecasts for Social Security indicate the program will lack enough to pay the full benefits beginning in the mid- to late-2030s..

“Discovering that we qualified for a particular benefit through Social Security was a pleasant surprise. We could see how that allowed us to create a filing strategy that brought the maximum benefit possible. This information has helped us be much clearer in our planning and decision making.” – M.L.

If nothing is done to remedy this situation, then the program would have to cut benefits across the board by about 21%. After that cut, the program would be solvent at that reduced payment rate as far as the eye can see. That includes payments to Millennials…and to people who aren't even born yet.

But here's the important bit to understand…

A 21% across-the-board cut would be painful and shocking—which is why it won't happen.

Remember, those 69 million current beneficiaries—they vote in huge numbers.

For as long as Social Security has been around, it's needed tweaks now and again to steer it along a more stable course. And we've made those tweaks.

Back in 1983, for instance, the Social Security Administration found itself facing an eminent shortfall. So what happened? Ronald Reagan appointed a commission to come up with a solution, which they did. Then he and House Speaker Tip O'Neill pushed the commission's proposals through Congress with strong bipartisan support. Crisis averted.

Now we find ourselves in a similar situation—not, in fact, nearly as pressing. Lawmakers will fix it, and they aren't going to do it by causing an uproar among tens of millions of voters. That would be bad politics.

I won't go into all the possible ways a fix could be made since I take you on the butler's tour in Social Security Secrets: How to Maximize Your Income for a Worry-Free Retirement.

But I will leave you with what Alan Greenspan said about this situation almost 15 years ago…

"If you get beyond the political rhetoric" and assembled a group to solve Social Security, "it would take them 15 minutes. It would take them 15 minutes only because 10 minutes was used for pleasantries."

I'll say it again: This "Social Security is bankrupt" line…this "sky is falling" hysteria…it's all bantered about for political gain.

If you take it to heart, you're almost certain to make poor decisions about your Social Security benefits that will cheat you out of funds you're due…funds that could make a huge difference in the quality of your retirement.

Don't be taken in.

Social Security will be there for you in full throughout your retirement. That's the smart bet. And you should plan accordingly.

I explain how, exactly, you do that in Social Security Secrets: How to Maximize Your Income for a Worry-Free Retirement.

You Need a Plan to Ensure a Better-Funded Retirement

I show you how to navigate your options…maximize the benefits due you…and position yourself to take best advantage of your retirement years.

And I’d like to send you a copy of Social Security Secrets: How to Maximize Your Income for a Worry-Free Retirement,

Inside my book you'll discover—

- How men very often inadvertently short-change their wives when it comes to Social Security benefits. (They wouldn't if they fully understood the impact of their claiming decisions. In Social Security Secrets: How to Maximize Your Income for a Worry-Free Retirement, the pitfalls are laid out clearly so you can plan wisely, whether you're single or married.)

- How to know if a “Tax Torpedo” is aimed at you. You can’t avoid it if you don’t know it’s coming! Turns out Social Security is treated in a peculiar way when it comes to taxes. Coupled with just a little additional income (say from IRAs or 401k accounts or rents, etc.), you pay zero federal income tax on it. But once that additional income reaches a certain level—and it’s not very high, in the $10k to $20k range—it not only adds to your taxable income, but at a certain point, it does so at a punishing, multiplied rate. So $1 of additional income could result in up to $1.85 of additional taxable income, even kicking you into a higher tax bracket! I lay out the strategies you need for reducing or even eliminating this “Tax Torpedo.”

- How certain wording can mislead you. For instance, it sounds like—over the long term—you're likely to pocket the same amount of funds whether you claim your retirement benefit as soon as you're eligible or you wait some years. But that's not necessarily right. Find out the real story…what it means for you…and how to plan accordingly.

- Can you work and collect Social Security or survivor benefits? “Yes” is the short answer. I’ll walk you through how the rules work, what tax implications you should be aware of, and how earning in your retirement years can, in fact, give you an advantage in the long run.

- How to ensure your deferred-tax savings don’t end up delivering your kids a massive tax bill. New rules stipulate that almost anybody except your spouse who inherits your deferred-tax accounts is required to draw the entire amount (including any earnings) down to zero within 10 years. That’s likely to hit your kids when they’re in their most productive earning years (that is: at the highest marginal tax bracket)! I’ll show you a strategy for making sure this doesn’t happen.

- The Social Security Administration employees know the facts. And they'll be as helpful as they can be. But they're busy. And they’re understaffed. In 2019, they handled 56 million calls on their national 800 number. Given your personal situation and your priorities, find out how you calculate the optimal time between ages 62 and 70 for you to begin claiming. Nobody is going to be as strong an advocate for your retirement income than you are. So let me help you get your ducks in a row.

- Not all Social Security benefits are automatic. For certain benefits, both you and/or your spouse must qualify and then file in a timely fashion—otherwise you could forfeit funds rightly due you. I show you the roadmap you need.

- Sometimes the Social Security Administration rules don't seem to make sense. For instance, while it can pay to get married, it can also be costly under certain circumstances to remarry. Better to live in sin? In some cases, the answer is "yes"—at least from a financial point of view.

- Divorced? You may well be eligible to claim spousal benefits based on your ex's work history…find out the parameters, the questions you need to ask, and how and when to file a claim.

- How to create a personalized claiming strategy that takes your current situation—as well as your long-term goals—into account to ensure you're activating your Social Security benefits in a way that'll provide for your comfort in retirement (and that of a widowed spouse, too, should that happen) and make sure you're not leaving money on the table.

- Why women need to be even more cautious than men when planning their Social Security claims in coordination with their draw on other financial assets. The tax implications can be significant for everybody—so smart timing is critical. I’ll show you how to keep more of what you deserve.

- How to use your Social Security claiming strategy to "super charge" your retirement and not only increase the amount of money you put in your pocket, but retire better…and quite possibly earlier…than you imagined you could.

- How to use the Social Security website to your advantage—what tools are there, how to make smart use of them, how to understand what the SSA is telling you, and how to use their calculator to run various “scenarios” for yourself so you can begin to see in concrete terms what your claiming options are and how each one delivers a different bottom line.

- How to arrange your affairs so your Social Security benefit rises over time—and is tax-free.

- How to integrate your Social Security strategy with tax-deferred withdrawals of your savings so you’re spending wisely and saving more.

- How—if your spouse receives Social Security retirement benefits—you can receive them, too...even if you’ve never worked under Social Security.

- And much, much more…

Smart Planning Isn’t About Social Security Alone

This book shows you how to consider your Social Security as part of your overall retirement plan—because if you look at it in isolation, you’re likely to shortchange yourself. I want to help you create a budget for the rest of your life.

Considering what you want your next decade or two to look like is a critical piece of the puzzle. And it has bearing on when you claim your Social Security benefit and when you spend any pre- or post-tax savings you may have in your nest egg.

You want to create a plan for yourself that soundly funds a life that looks the way you want it to and will allow you to live worry-free. Rest assured: You can do that—even on your Social Security alone.

Social Security Secrets shows you how. Inside, with my guidance, you’ll consider how you want to spend your time: Will you travel, will you work, will you do both? And, then, with an end goal in mind, you can begin to put together a sound plan to fund that vision.

For example, you should know: Social Security usually offers a pretty sweet tax deal. But not always. Few people have a good sense for how benefits are taxed and, as a result, retirees often pay more in tax than they need to. (Sometimes thousands of dollars a year more.)

In Social Security Secrets, I show you how various financial elements at your disposal can “play nicely” together so you can save (and spend) with confidence. And enjoy a long and worry-free retirement.

…in fact, there's so much more in this book, I don't have the space to go into all of it here.

Give This Valuable Book a Try

Fundamentally, this book is about value.

It shows you how to ensure you're not leaving money that's rightfully yours on the table.

And it explores just how valuable your Social Security benefits really are. Consider, for a minute, that if you were to purchase from an insurance company an annuity that paid you a monthly $2,000 (adjusted for inflation) from age 66 on—that annuity would cost you about $550,000 if you’re male or $600,000 if you’re female.

My point is: Your Social Security benefit really IS valuable. For many people—it's worth more than their savings and more than their home.

So you can see why I believe that it deserves a measure of attention and management. You wouldn't leave a nest egg worth more than half a million dollars to chance. Nor should you neglect your Social Security benefits.

You need a smart claiming strategy, and that's exactly what I map out for you in Social Security Secrets: How to Maximize Your Income for a Worry-Free Retirement.

Plus, Discover How to "Super-Charge" Your Retirement Benefits

There's something else important I talk about in my book—a way to "super charge" your Social Security benefits and use these funds to gain not only a better retirement…but potentially an earlier (and longer) one, too…

I'm talking about a way to effectively double, or even triple your disposable income in retirement so you can retire sooner…and better…than you ever thought you could.

Let me explain.

There's no question that one of the best ways to stretch your Social Security benefits is to make sure you're claiming every cent you're due. And that means having a thoughtful claiming strategy in place. As I said earlier, experts say that 96% of retirees aren’t getting as much as they could. The average retiree household leaves $111,000 on the table over the course of their retirement. Money they simply never see.

You don't want to be in that group.

In addition to having a smart claiming strategy, you can ensure your benefits go further by lowering your cost of living. You see people do this all the time in retirement. They downsize to a smaller property to free up assets and simplify life.

And of course, depending on your circumstances, if your retirement income is modest (maybe, in fact, limited to your Social Security benefits alone), then you could find yourself cutting back…skimping a little…making sacrifices.

But here's the good news…

When you "super charge" your Social Security, you don't have to give up a single thing. In fact, you could retire in luxury.

“We want to thank you for your time and effort in explaining the Social Security system...The charts you provided ...for early filing and waiting until we reached the best time to start collecting our Social Security helped make our decision on when and how to file very easy.” – K.K.

Here's how it works: You can access your Social Security benefits from all over the world. And this gives you options for retirement living that you may never have considered before. Or thought possible.

If you like the idea of traveling in retirement…if you'd like a little adventure in your life…if you like the prospect of never having to worry about money again…

…then you should consider "super charging" your Social Security.

You see, when you take your Social Security income to the right places overseas…rather than trim your lifestyle in retirement, you can watch it expand.

And this is something you could do for just a year or two if you wanted—buying yourself some big-adventure, low-cost living abroad, which could allow you to delay taking your Social Security benefit until the time is right for you.

Now yes, I realize we’re all hunkered down for the moment. But this craziness will pass, and while you sit it out is a smart time to not only dream about pretty, safe, low-cost escapes, it’s also a time to learn about where they are...

In the Best-Value Places Overseas, You Can Live Twice as Well for Half as Much

In the best-value destinations beyond our borders, you can live way better than you do at home, for half the price. That's because your dollars can go much, much further than they do in the States.

And that can hand you the power to not only retire better—but to retire sooner, too.

In welcoming, beautiful, good-value destinations from Latin America to Europe to Southeast Asia, you can live like a king on your Social Security income alone.

You see, in places where the cost of living is so much lower than it is in the States, you could have excellent healthcare and insurance you can afford, a housekeeper to clean for you, funds to travel when you feel like it and eat out whenever you want. You could live right on the beach with a water view.

A lifestyle that back home would cost you six figures can be yours on your Social Security income alone in the best-value places overseas.

Take Ed and his wife, Olga, who traded a stressful, expensive life in Pennsylvania for a better, lower-cost one in an arts-rich city overseas.

"Our only income is my Social Security, but we're living better than we ever have before," says Ed.

"We pay $350 a month in rent for our new, 1,616-square-foot, three-bedroom, two-bathroom apartment. And the monthly cost for utilities is equally low: Electricity and trash removal, $12.70…water, $6.61…propane for hot water, gas dryer, and gas stove, $4.64…phone/internet, $30.11.

"We have a full-time maid who does all our chores and a gardener who cares for the yard. We spend our days going to the gym, taking Spanish classes, horseback riding, hiking nearby volcanoes, going to the beach and exploring the country. "And we do all this for less than half the cost of a moderate lifestyle in Atlanta." – J. and N., maximizing their retirement overseas

"Today, we live in this beautiful, affordable city, surrounded by its many majestic churches and old buildings, and enjoy a wonderful climate.”

They say they stay entertained by going to symphony performances, museums, theaters, and exploring historic landmarks.

Theirs is one of thousands of stories of people like them who've chosen to "super charge" their Social Security benefits and retire better…and earlier…overseas.

The bottom line is this: On as little as $1,700 a month, housing included, a couple can live very comfortably in the best-value locales overseas, and a single person— on even less.

This book is all about giving you options in retirement…options that hand you more money and more possibilities for living a better, richer, freer—worry-free—life. A life where you're in control of what your retirement looks like…

Just one important piece of intelligence you gain in Social Security Secrets: How to Maximize Your Income for a Worry-Free Retirement…just one single recommendation…could be worth tens of thousands of dollars to you.

But I'd like to send you this book for just $24.95 plus shipping.

That's less than you'd pay for a pizza and a couple of beers. Yet it could completely change the course of your retirement…for the better.

And that's not all.

Request your copy of Social Security Secrets now and I'll send you four more valuable resources as well.

They're all yours with my complements, and they're not available any other way…

I'll Also Send You Two FREE Gifts

Because I want you to be as prepared as possible to get the most out of your retirement years—not only in the income you receive, but in the quality of the life you enjoy—I want to send you four more special gifts when you request your copy of Social Security Secrets: How to Maximize Your Income for a Worry-Free Retirement today…

FREE GIFT #1: BONUS CHAPTER: How to Grab an EXTRA Social Security Payout of up to $50,000

I mentioned up front here that a specific provision in play right now in 2024 is paying out as much as an extra $50,000 to qualifying recipients. You have limited time to figure out if you could be due the maximum funds under this specific provision.

If you qualify for these extra Social Security benefits—and hundreds of thousands of people do—you have to request them in a timely manner. If you don’t, you could find you’re out funds that could have been yours.

This special Bonus Chapter—which I'll deliver immediately via email—tells you exactly how this benefit works, who qualifies, and how to request the extra payout due you should you be one of the many people who qualify for this special benefit.

When you request your copy of my book now, it’ll take a little while to wend its way to you in the mail—but I’ll send you details on how to access this Bonus Chapter so you’ll have it almost immediately and can take action.

FREE GIFT #2: The Workbook—Nuts and Bolts for a Luxury Retirement on Your Social Security

There are a series of questions you'll need to answer and calculations you'll need to make in order to come up with a Social Security claiming strategy that makes the right sense for you. Social Security is complicated—but I’ve broken it all down so it's simple and straightforward for you.

This digital workbook—a companion guide to Social Security Secrets: How to Maximize Your Income for a Worry-Free Retirement —gives you the worksheets to fill out and resources you can use to get answers to questions, and more…

And when you take me up on this special offer today to get your own copy of this important book, I’ll toss in this second bonus, FREE, as well.

FREE GIFT #3: Special Report: 8 Countries Where You Can Live Like a King on Your Social Security Income

My publisher, International Living, is in the business of showing people how to upgrade to a better life while spending less. Maximizing your Social Security benefits…that's just one piece of it—the piece they invited me to explore in my book for your benefit. But you can maximize your lifestyle too.

In some places, you really can enjoy a Rolls Royce quality of life on a run-down Chevy budget. The kind of high-end living that might set you back $10,000 or $15,000 a month in a big city at home could be one-tenth that in the right places overseas. And the editors have pulled together a list I think you’ll find enlightening in these troubled times.

In one spot we like, for instance, expats Keith and Lisa rent a stylish three-bedroom, three-bath sea-view apartment of 2,200 square feet for about $950 a month. It comes with a shared pool and gym and sits on a private beach. Keith says, “A similar apartment in Los Angeles or Miami would cost at least $8,000 per month .” When you “super charge” your Social Security and take it with you overseas, it really can allow you to live better, retire sooner, and get more out of your “golden years.”

This special report is also yours—FREE—when you order my book today.

FREE GIFT #4: How to Take Your Social Security Overseas: Useful Resources, Answers to the 5 Most Common Questions, and Stories from People Who Have Done It

It’s straightforward—and completely legal—to take your Social Security with you overseas. In fact, more than half a million people do it already. And lots more simply continue to bank at home while they enjoy living well for less abroad for all or part of the year.

Point is: Your Social Security funds are yours, and you can spend that money in any way—in any place—you like, wherever in the world you choose to spend time.

Still, if you’re intrigued by this option, you probably have a few questions. And since we’re in the business of educating you about your options, we answer the most common ones in this special bonus report, which is also yours—at no cost—with this special offer.

Our Guarantee

So that's four free gifts: the Bonus Chapter, the workbook, and the two special reports. As I said, you can have all of these gifts at no cost—via email—when you order a copy of Social Security Secrets: How to Maximize Your Income for a Worry-Free Retirement to be sent to your home, now.

Simply click the "Add to Cart" button to get your paperback copy on the way to you immediately for just $24.95 plus shipping.

Once you’ve received it, I believe you’ll be impressed. But, if you’re not, please send it back for a no-fuss refund, minus the shipping fee. The bonuses are yours to keep, forever—my gift to you.

We’re Giving This Package Away for a Reason…

I really am on a mission to set the record straight about retirement today. So many people feel as if they won't ever be able to retire. Or, if they do retire…that they'll have to endure a lifestyle that's much less comfortable than the one they'd always hoped for.

But it's just not true.

You have way more control over the amount of income you receive from Social Security than anybody ever tells you. Experts estimate that almost every retiree household today is leaving money on the table—an average of $111,000 per household over the course of their retirement. They just don't claim it, because their timing is off—they make a claim too early—or else, they’re eligible for additional funds, based on their specific situations, but they don’t realize it. I’d like to make sure that doesn't happen to you. This book addresses not only Social Security claiming strategies—but it shows you the full context in which you should consider your Social Security. It talks about how Social Security fits into your bigger retirement-planning task and shows you ways to think about how you can put it to work for you in the most powerful ways.

I believe strongly in the importance of putting in place a sound claiming strategy that allows you to maximize your Social Security and retire worry-free.

And I believe my book is the most effective way to get this intelligence into your hands.

The bottom line is this:

You get all the intelligence you need about how to put a smart Social Security claiming strategy in place in the book, Social Security Secrets: How to Maximize Your Income for a Worry-Free Retirement.

Simply click the Add to Cart" button to get your paperback copy on the way to you immediately for just $24.95 plus shipping.

Again, you'll receive digital copies of the Bonus Chapter (with all the details of the claiming strategy that is paying out as much as $50,000 to each qualified person) and the workbook, after you place your order.

Then, soon after, a printed version of Social Security Secrets: How to Maximize Your Income for a Worry-Free Retirement will arrive at your home in your mailbox.

I look forward to sharing all this intelligence with you—and to helping you understand the easy ways you can increase your income (and improve your lifestyle) in retirement.

Sincerely,

Steve Garfink

Author, Social Security Secrets: How to Maximize Your Income for a Worry-Free Retirement

(and long-time International Living subscriber)

October 2021

P.S. We'll toss in something extra when you click below right now to order your copy of Social Security Secrets: How to Maximize Your Income for a Worry-Free Retirement and your free bonuses.

We'll not only drop a copy of the book in the mail to you. But we'll email you a link to my book in digital form, too. That means you'll have almost instant access to it and can read it online or download it to your computer or tablet.

Click on "Add to Cart" to let me know where to send your package.